Once shunned, activist investors are now seeing a 'wave of change' in Japan - 8 minutes read

A Kyushu Railway Co. 800 series Shinkansen bullet train arrives at Kurume Station in Kurume City, Fukuoka Prefecture, Japan, Oct. 11, 2016.

Akio Kon | Bloomberg | Getty Images

Activist investing in Japan is on the rise, a gradual but marked change for a country long hostile to "foreign vultures" thought to be solely motivated by short-term profit.

Jeffrey Ubben's ValueAct will soon have a representative, Robert Hale, on the board of camera company Olympus and Daniel Loeb's Third Point is reportedly reinvested at entertainment giant Sony. That's not to mention King Street Capital Management's successful effort to push electronics maker Toshiba to put even more international investors on its board.

And for Fir Tree Partners, progress has been slow but steady.

"There is a wave of change in Japan," Fir Tree partner Aaron Stern told CNBC. "I see it just in the level of engagement: I used to be meeting with investor relations. Now I'm meeting with CEOs."

The New York-based fund manager has for years lobbied some of Japan's largest conglomerates to rethink how they spend their money. While the firm more often keeps its investments private, it has taken its campaign at one of Japan's largest railway operators, JR Kyushu, public.

Though the activist's bid for a board shake-up — as well as a 10% buyback — may seem unremarkable to an average American investor familiar with longtime Wall Street personalities like Starboard Value's Jeff Smith and Pershing Square's Bill Ackman, even glacial progress in Japan represents a big shift in the Land of the Rising Sun.

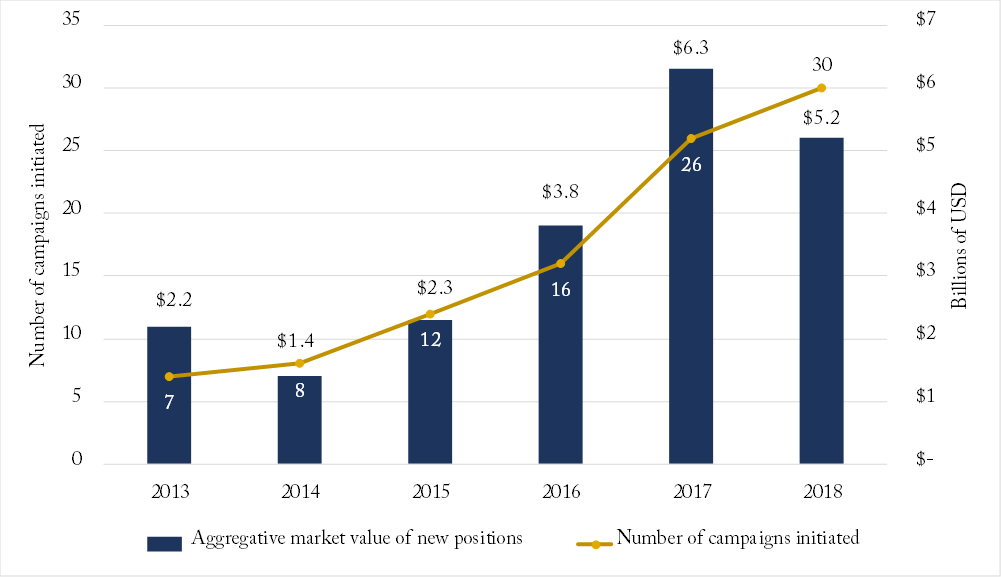

Source: Lazard; Activist Insight; FactSet

While at one point in the not-so-distant past one could count the annual number of Asia-Pacific campaign launches on a single hand, investor activism in the region has steadily climbed in recent years. From a low of seven campaign launches in 2013, the number of new engagements rose to a high of 30 in 2018, according to research conduct by Jim Rossman, head of Lazard's shareholder advisory unit.

'You have to do this on the street'

The uptick in campaigns has naturally buoyed the amount of capital that funds have tied up in the region, which summed north of $5 billion in 2018.

That's "one thing about being a foreign fund and trying to rattle the cages: You have to do this on the street in Japan — in order to get support, you have to get individual support and that's expensive and time-consuming," said NWQ Investment Management analyst Peter Boardman.

Figures reflecting an uptick in investor activism in Japan can be tied to a pivot in political policy, Boardman said, noting Prime Minister Shinzo Abe's efforts to encourage corporate engagement. That back-and-forth dialogue between shareholders and company management will be critical, Abe believes, if the country's younger generations hope to come close to paying for the ballooning health-care costs associated with a rapidly aging population.

But while some data suggest progress, Japan is still in the early innings of a pivot toward diverse boards. More than 92% of directors at Japan's TOPIX 500 companies are Japanese men, according to Jefferies. The brokerage also found that of inside director seats, 98% are Japanese men, only 0.5% are women, and 1.7% are foreigners.

There were only 323 women in total on the boards of TOPIX 500 companies in 2018, which represents 0.6 women on an average 11-person board, Jefferies analysts found.

Still, Abe's policy shift has translated into momentum for domestic and foreign activist funds at the margin.

"We're in a period in Japan where the government is our best friend," Boardman said. "All the pension funds used to be long bonds and now rates are at zero. You need to invest in equity or equity-like products."

"The demographics are demanding companies to start thinking long term, start thinking about return on investment," he added. "Management wants to keep cash on the balance sheets because it's not sure about future growth." NWQ Investment Management was a stakeholder in JR Kyushu until 2017, when it dissolved its holding.

Boxcar bout

For Fir Tree, founded in 1994 by Jeff Tannenbaum, its campaign at JR Kyushu has been a multiyear battle centering on the company's use of cash.

Those in favor of changes at the company say it's unclear how its investments in noncore hotel and hospitality businesses add long-term value, especially in geographies beyond the Japanese island of Kyushu. In addition to serving as train stations, the company's large transit hubs often include a wide range of commercial real estate, including shopping centers, office buildings and hotels.

"We've had very good dialogue with management: we've been meeting with the CEO, some board members and other senior executives on quite a frequent basis over the last few years," Fir Tree's Stern told CNBC. "While they did reject our call for a three-committee structure for the board, they are going a step in the right direction by trying to set up a nominating committee to bring in independent directors."

JR Kyushu became Japan's first railway listing since the 1990s in 2016 as the government privatized part of its railway system on Kyushu island, a popular tourist destination and home to the city of Nagasaki. One of the six major bullet train operators once owned by Japan, the company raised around 416 billion yen (about $4 billion) for its IPO, promising investors an attractive dividend of about 75 yen, a yield of about 3%.

But for Fir Tree, which has been a shareholder in JR Kyushu since its IPO, a meager 6% climb in the stock over the last few years and a general lack of transparency has been an impetus for a more activist approach.

"The concerns revolve around why they are investing in areas outside their main region. If they have excess capital, why don't they return it to shareholders?" Boardman said. With Japanese interest rates at the zero bound, "why not maintain your leverage and return more to investors?" he said. "It makes a lot of sense."

JR Kyushu recently acquired an apartment complex in Bangkok and has poured funds into new hospitality brands and in luxury hotels in Tokyo. And while Fir Tree may not necessarily oppose the company's move to invest, more disclosure about how the company plans to generate returns on its real estate holdings may be helpful.

The fund has also urged the board to consider a 10% share buyback program, a stock compensation plan for directors and a slate of directors with more industry expertise. It's nominated three directors to the company's 16-member board, with Toshiya Kuroda, J. Michael Owen and Keigo Kuroda.

Those changes, combined with a more fundamental rethinking of how to value the company's assets, Stern believes, could double JR Kyushu's stock price. Fir Tree owns about 6% of JR Kyushu according to the fund's recent press releases.

Activists making moves

The Seven Stars in Kyushu cruise train

Source: Luxury Travel Intelligence | VeryFirstToKnow.com

At JR Kyushu, top proxy advisors Institutional Shareholder Services and Glass Lewis both support the fund's push for reform and encouraged investors to consider outsider ideas when they vote at the company's meeting on June 21.

"JR Kyushu is a company with heavy exposure to real estate (yet, no net debt) that the market values at low multiples vs. peers with relatively similar business profiles," ISS said in a presentation published Wednesday. "Given these factors, and our support for the dissident's share buyback proposal, the election of two additional directors with real estate and capital allocation experience would help reevaluate current and future investment plans."

Though ISS recommended shareholders vote for Kuroda and Kuroda, Glass Lewis advocated for all three nominees and for Fir Tree's director compensation proposal. Rick Gerson's hedge fund and fellow JR Kyushu stakeholder, Falcon Edge Capital, also voiced support for some of Fir Tree's initiatives on Wednesday.

But the company has thus far opposed key tenants of Fir Tree's suggestions, saying that it needs to keep cash on hand in case of a market downturn and to fuel its other initiatives.

"The Shareholder Proposal to Conduct a Share Buyback is the proposal to use large-scale debt financing to implement the share buyback, and it ignores financial soundness and is aimed solely at short-term shareholder returns, which would weaken JR Kyushu's ability to respond to the business risks," the company said a press release.

Still, Stern was optimistic, saying that his fund's proposals represent a good compromise between the company's desire for financial flexibility and a duty to shareholders to maximize returns.

"It's a very good compromise," he said. Fir Tree's nominees "could work well with the existing board and have experience in Japan."

"It's clear shareholders want more," he said.