Chairman Powell Moves Toward My Recession Prediction And Helps Trump Trade War - 12 minutes read

Chairman Powell Moves Toward My Recession Prediction And Helps Trump Trade War

Chairman Powell Moves Toward My Recession Prediction And Helps Trump Trade WarIt turns out tariff wars are trickier than Trump said they were, which is partly why Trump is constantly cudgeling Fed Chair Jerome Powell to lower interest.

The bears that are gathering will soon enough be picking flesh off the sun-bleached bones of this market. Even the Fed Chair, who usually does all he can to avoid dismal pictures and to sound optimistic, is finally talking downcast about the US economy.

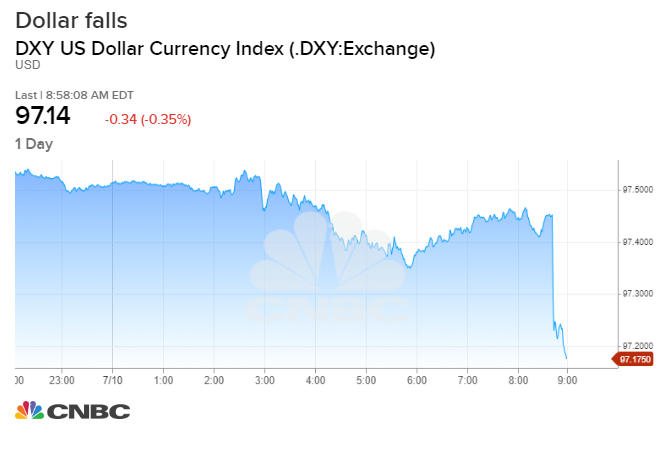

He didn't do much, but Powell genuflected in Trump's direction, giving him a nudge where he needed it in trade. Powell's congressional comments today helped Trump out a little with his trade-deficit problem by causing the dollar to plunge in value:

Since Trump has been in office, the trade deficit has widened by 25% (as has the US budget deficit). The trade deficit is widening because countries are importing fewer US goods and because they are lowering the value of their currency against the dollar, and we measure trade in dollars. As foreign currency devalues, it takes fewer of those dollars to buy the same amount of goods.

That devaluation of foreign currencies is good for US consumers, but bad for US exporters because the price of their goods in foreign currencies goes up because they start out being built and priced in dollars, so they sell fewer goods abroad. It's also bad for US trade statistics. When other nations lower their currency, the lower price of goods in US dollars increases the amount of goods on the foreign side of the ledger than the US imports, widening the trade deficit.

It turns out tariff wars are trickier than Trump said they were, which is partly why Trump is constantly cudgeling Fed Chair Jerome Powell to lower interest (as that correspondingly has the effect of devaluing the dollar on foreign exchanges … as other nations are doing). It helps us in a trade war by getting into a currency war. The enemy fights back, as it turns out, and so far the enemy is winning in terms of the trade balance sheet.

Powell's remarks also helped Trump by giving his prize badge, the stock market, a boost. I had said in a comment on this site yesterday, that I anticipated the S&P would break briefly through its 3,000 barrier, and it did that intraday today, so that didn't take long. (Whether it closes there, having settled back beneath that level, remains to be seen.)

My comment was actually in respect to my agreement with nearly everyone else's opinion that the most-likely scenario for July is that the Fed will lower interest rates by 0.25% near the end of the month. That, I said, will give stocks a brief bump - not much of one because it is already priced in; but there is always a little hallelujah dance when the moment arrives and does what it was supposed to - a relief rally as the pressure of waiting and wondering is lifted.

Then reality sets in a day or two later. My most-likely scenario for June and July has been that Trump and Xi would agree to continue talks but not get much accomplished and that Powell would talk the market up and will ultimately give the 0.25% rate increase the market is demanding. I've never believed he has the courage to crash the market (the worst-case scenario I presented for June and July).

However, I have said all along, what happens economically in the run-up to that big day and in the days after that rate cut matters more because the rate-cut is already priced in. That's why it's only going to deliver a bump.

What happens during those days leading up to and after the Powell put is going to be increasingly bad economic news. In fact, that news, I've said, will press Powell into delivering the rate cut that both the bond market and stock market are demanding (which is why I moved some of our own money into bonds this month). That news will be trouble for stocks and probably good for bonds (lowering yields, which makes the bonds that are already in bond funds worth more because they have higher yields). Money moving out of stocks could seek safe haven in bonds, pressing bond yields down ever more.

Under the new economic paradigm, the Fed single-handedly created during its recovery regime, bad economic news is good news for stocks here in Wonderland because it assures more free Fed funds are coming soon. Since free money happens quicker and easier than earning money the hard way, that is currently all investors care about. That is, until things go so bad with the economy that there is no way to keep up the pretense that business is going along with all the falderal. Earnings are about to change the picture.

That is where Powell is finally winding up, just as I said he would be as July wore on. He is starting, at last, to see the economy my way! His talk shifted notably this week from past months of saying the economy was sound and expanding to sounding concerned about growing recessionary forces. Here are the specific concerns Powell laid out. Most of them are concerns he is expressing for the first time:

In other words, Powell sees that DEFLATIONARY pressures have returned. Earlier in the year he saw inflation as being above the Fed's 2.0% target, so he spoke in terms of a "symmetric target," meaning - as I pointed out in one of my Premium Posts titled "Teasing out the Fed's Big Plan for our Future" - the Fed would be aiming for inflation above 2% in what Powell termed a "make-up" strategy for the years when the Fed couldn't get inflation up to save its life. The Fed hoped to run the economy hot.

Powell sees that hope rapidly fading away now, and that is much greater incentive for him to give that rate cut and to restart quantitative easing, as I've said for years the Fed will have to do when it realizes its great recovery is failing due to its Great Recovery Rewind (balance-sheet reduction). Good unemployment numbers, especially now that they are hinting at turning the wrong way, are not going to dissuade the Fed from aiming to raise inflation by lowering interest rates.

Declining inflation provides the ready excuse for Powell and the boys and girls at the Fed to do what stocks and bonds are both demanding in order to avoid a tantrum they do not want to be seen as being responsible for. I said in earlier comments, that if Powell is leaning toward giving the market what it demands, look for his comments to start focusing on falling inflation so that Powell can say at the end of July the Fed is cutting rates due to inflation, rather than due to being the market's slave and Trump's boy. Now, here we have it:

Just from this tease, stocks rose and bond yields, which had been rising due to stronger job numbers, settled back down today. All was made well as Papa Powell comforted his markets. Where the market was recently concerned that a blip up in job number might keep the Fed from doling out cheap money, those concerns are now assuaged:

The other growing concern Powell fixed on was trade. I said earlier this month Trump would keep trade concerns on the Fed's front burner through July (even if he could solve them, which he probably can't) in order to extract his rate cut from Powell. Powell is now paving a path to capitulate:

Powell hit the drum numerous times on both low inflation and rising trade-war problems. In fact, he hit the trade note more times than any other thing he talked about in both his own speech and during questions and answers; and he didn't just go there when Democrats led him that way with questions. So, Powell not only laid a clear path to rate cuts based on the Fed's inflation mandate but also laid a path to blame the need for those cuts on the Trump administration by basing growing economic troubles on Trump's trade war, rather than on Fed monetary tightening.

Business conditions are also declining, which Powell tied to trade problems, and that is resulting in lowered capital investment, certainly a recessionary move. That has now caught Powell's eye, too, just as I've said recessionary forces would start to do in July:

Finally, Powell noted slower growth in economies all over the world as a pressure on the US economy.

In all, CNBC described our reserved chairman's testimony as striking "a downbeat tone," which perfectly sets the tone for his rate cut; but it also means the rate cut will be happening, as I've been saying for months would be the case, as recessionary winds in the general economy begin to blow. And, no matter how much good news is bad news here in Wonderland, no stock market has ever weathered a recession well.

As I've said, the dizzy stock market looks at economic weakness as hope of dope from the Fed's free dispensary, and it will be that for sure; but what the market is completely failing to grasp is that years of Fed meds boosted the market AFTER it has already plunged into the basement. It is entirely different when the Fed starts down the interest-rate-cutting path after the end of a long expansion. It is one thing to boost a market valued low because it has already collapsed and to do it as economic times are starting to recover. It is another thing entirely to boost the stock market when values are at record heights and to do so as the economy is falling.

Put your money there if you want. It should be good for a bounce this month, but good luck with that later in the summer as all the forces Powell is now finally starting to openly fear continue to build … exactly as you've been reading about here all year.

As the bulls crack the corks on their champagne bottles when the Fed makes it first rate cut in years at the end of July, just remember how the Fed's first rate cuts in 2000 and 2007 turned out.

Here's a graph I've presented more than once as I've built my case for a summer recession and for the Fed's first increase being the perfect start to such a recession. Notice where the Fed's first rate cuts after a long period of rate increases typically times out and how far the Fed has to keep cutting before the attending recession ends:

You don't get nicer correlation than that! Maybe that will stuff the cork back in your champagne and save you from a major hangover later. Remember, drinking and cliff-climbing don't mix.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Source: Seekingalpha.com

Powered by NewsAPI.org

Keywords:

Recession • Trade war • Tariff • Chair of the Federal Reserve • Interest • Hunter-gatherer • Market (economics) • Chair of the Federal Reserve • Economy of the United States • Colin Powell • Donald Trump • Colin Powell • United States Congress • Balance of trade • United States dollar • Balance of trade • National debt of the United States • Balance of trade • Goods • Value (economics) • Dollar • Dollar • Currency • Dollar • Goods • Devaluation • Currency • Goods • Consumer • United States dollar • Export • Price • Goods • Currency • Goods • Trade • Lower house • Currency • Lower house • Price • Goods • United States dollar • Goods • Foreign trade of the United States • Balance of trade • Tariff • Chair of the Federal Reserve • Lower house • Interest • United States dollar • Trade war • Currency war • Balance of trade • Balance sheet • Stock market • Interest • Hallelujah (Leonard Cohen song) • Worst-Case Scenario series • Economy • Bond market • Stock market • Money • Stock • Yield (finance) • Yield (finance) • Money • Stock • Bond (finance) • Yield (finance) • Economy • Federal funds • Free Money (film) • Deflation • Inflation • Federal Reserve System • Federal Reserve System • Inflation • Inflation • Federal Reserve System • Economy • Incentive • Interest rate • Quantitative easing • Federal Reserve System • Balance sheet • Goods • Unemployment • Federal Reserve System • Inflation • Interest rate • Inflation • Federal Reserve System • Stock • Colin Powell • Market (economics) • Inflation • Federal Reserve System • Inflation • Market (economics) • Slavery • Donald Trump • Stock • Bond (finance) • Employment • Market (economics) • Market (economics) • Money • Trade • Inflation • Trade war • Democracy • Colin Powell • Federal Reserve System • Inflation • Presidency of Donald Trump • Economy • Trade war • Federal Reserve System • Money • Business • Investment • Economic growth • Economy • Economy of the United States • CNBC • Stock market • Recession • Stock market • Cannabis (drug) • Meds • Interest rate • The Economic Times • Champagne • Graph (discrete mathematics) • Recession • Recession • Recession • County Cork • Champagne • Hangover • Seeking Alpha •